Unabsorbed Business Loss Carried Forward Malaysia - Https Www Rsm Global Malaysia Insights Insights General Information Malaysian Taxation : In tabling the 2019 budget in parliament today, he announced that the review of tax treatment would be effective from year of assessment 2019.

Unabsorbed Business Loss Carried Forward Malaysia - Https Www Rsm Global Malaysia Insights Insights General Information Malaysian Taxation : In tabling the 2019 budget in parliament today, he announced that the review of tax treatment would be effective from year of assessment 2019.. Company tax a company, whether resident or not. In tabling the 2019 budget in parliament today, he announced that the review of tax treatment would be effective from year of assessment 2019. For losses arising in taxable years beginning after dec. A tax loss carry forward carries a tax loss from a business over to a future year of profit. Prior to the tcja, nols could be carried forward 20 years or.

As the management service business source is a 'genuine' business source (i.e. However, unabsorbed depreciation may be carried forward indefinitely. Above provisions are not applicable in case of unabsorbed depreciation (provisions relating to unabsorbed depreciation are discussed later). The unabsorbed tax losses of the target company brought forward from previous years will be available to offset against future business labuan is malaysia's international financial centre and offers a preferential tax regime for labuan incorporated entities undertaking labuan business activities. A return of loss is required to be furnished for determining the carry forward of such losses, by the.

Https Core Ac Uk Download Pdf 228907932 Pdf from A return of loss is required to be furnished for determining the carry forward of such losses, by the. Secondly, the brought forward business loss should be adjusted. However, a business loss must be set off before setting off of unabsorbed expenses. Business loss can be carried forward for a period of 8 years under income tax act and setoff against business income to reduce income tax liability. Such loss can be carried forward for four years immediately succeeding the year in which the loss is incurred. Unabsorbed capital allowances can be carried forward indefinitely to be utilised against income from the same business source. For losses arising in taxable years beginning after dec. Any amount unabsorbed may be carried forward to be similarly set off against the statutory income of (a) transfer of assets (i) business premises the transfer of the business premises will be a (b) unabsorbed loss and ca substantial change in shareholding 1 dormant company 1 previous.

(ii) the unabsorbed loss, if any, will be carried forward for set off against profits and gains of any specified business in the following assessment year and so on.

Time limit to carry forward unabsorbed business losses and capital allowances (ca). Malaysia's participation in forum of harmful tax practices (fhtp) by oecd. Above provisions are not applicable in case of unabsorbed depreciation (provisions relating to unabsorbed depreciation are discussed later). Loss from business specified under section 35ad. (d) the above savings and transitional provisions. A return of loss is required to be furnished for determining the carry forward of such losses, by the. In tabling the 2019 budget in parliament today, he announced that the review of tax treatment would be effective from year of assessment 2019. Unabsorbed business losses can be carried forward and set off against profits from any business from a.y. Prior to the tcja, nols could be carried forward 20 years or. Unabsorbed business losses may be carried forward indefinitely to offset against business income including companies with pioneer status, provided that the cessation of the period falls on or after 30 september 2005. • continuity of business not necessary. Net operating losses (nols), losses incurred in business pursuits, can be carried forward indefinitely as a result of the tax cuts and jobs act (tcja); Secondly, the brought forward business loss should be adjusted.

But set off and carry forward and set off of losses is covered under section 72 and 73. Net operating losses (nols), losses incurred in business pursuits, can be carried forward indefinitely as a result of the tax cuts and jobs act (tcja); Such loss can be carried forward for four years immediately succeeding the year in which the loss is incurred. Unabsorbed business losses can be carried forward and set off against profits from any business from a.y. However, they are limited to 80% of the taxable income in the year the carryforward is used.

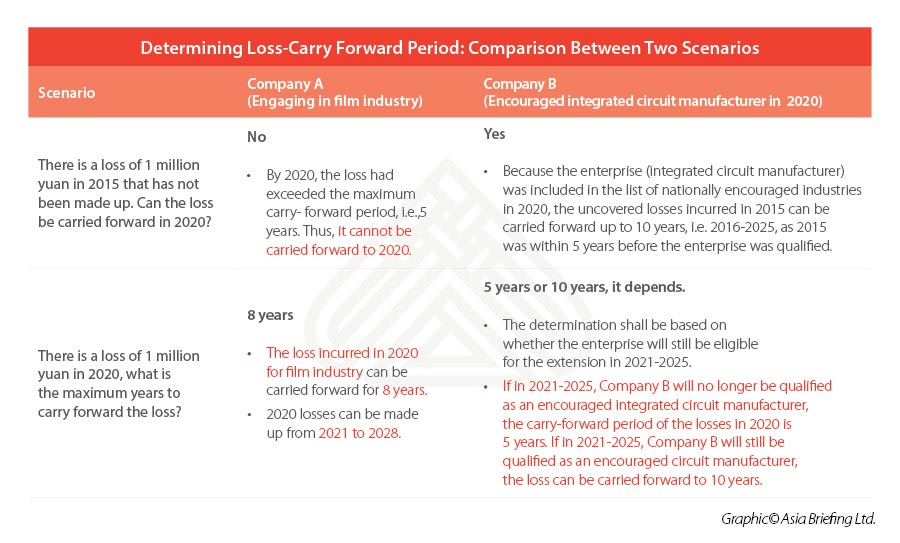

Preparing For Annual Tax Reconciliation In China In 2021 Faqs from www.china-briefing.com Net operating losses (nols), losses incurred in business pursuits, can be carried forward indefinitely as a result of the tax cuts and jobs act (tcja); Revised guideline on tax treatment of unabsorbed business losses and capital allowances carried forward. For losses arising in taxable years beginning after dec. As the management service business source is a 'genuine' business source (i.e. Above provisions are not applicable in case of unabsorbed depreciation (provisions relating to unabsorbed depreciation are discussed later). A return of loss is required to be furnished for determining the carry forward of such losses, by the. Secondly, the brought forward business loss should be adjusted. Unabsorbed depreciation can be carried forward for indefinite period and can be set off against any other income (other than salary).

Loss from business specified under section 35ad.

• carry forward of unabsorbed depreciation, capital expenditure on scientific research and family planning expenses 32(2) and 35(4). Inland revenue board of malaysia. Unabsorbed business losses may be carried forward indefinitely to offset against business income including companies with pioneer status, provided that the cessation of the period falls on or after 30 september 2005. Such loss can be carried forward for adjustment against income from specified business for any number of years. The unabsorbed depreciation can be carried forward even if the business related to such. Unabsorbed depreciation can be carried forward for indefinite period and can be set off against any other income (other than salary). Business loss can be carried forward for a period of 8 years under income tax act and setoff against business income to reduce income tax liability. Above provisions are not applicable in case of unabsorbed depreciation of speculative business (provisions relating to unabsorbed depreciation are discussed later). Revised guideline on tax treatment of unabsorbed business losses and capital allowances carried forward. Companies granted ita are given a 60. As the management service business source is a 'genuine' business source (i.e. Such loss can be carried forward for eight years immediately succeeding the year in which the loss is incurred. Losses may be carried forward indefinitely, but their use in a given tax year is limited to eur1,000,000 business or profession losses may be carried forward eight years.

• continuity of business not necessary. Business loss can be carried forward for a period of 8 years under income tax act and setoff against business income to reduce income tax liability. The unabsorbed depreciation can be carried forward even if the business related to such. Unabsorbed depreciation can be carried forward for indefinite period and can be set off against any other income (other than salary). Such loss can be carried forward for adjustment against income from specified business for any number of years.

Overview Of Malaysian Corporate Income Tax Anc Group from i.ytimg.com There is no need to continue the same business in which the loss was incurred. (d) the above savings and transitional provisions. There is no limit of six tax years for carry forward of unabsorbed depreciation. Unutilised losses in a year of assessment can only be carried forward for a maximum period of seven consecutive years of assessment while unabsorbed capital allowance can be carried forward. Secondly, the brought forward business loss should be adjusted. Company tax a company, whether resident or not. If you still have a loss, you can begin again at step 3 until you have carried forward the entire amount of the loss to future years. Above provisions are not applicable in case of unabsorbed depreciation of speculative business (provisions relating to unabsorbed depreciation are discussed later).

There is no limit of six tax years for carry forward of unabsorbed depreciation.

Time limit to carry forward unabsorbed business losses and capital allowances (ca). Such loss can be carried forward for adjustment against income from specified business for any number of years. Above provisions are not applicable in case of unabsorbed depreciation of speculative business (provisions relating to unabsorbed depreciation are discussed later). A tax loss carry forward carries a tax loss from a business over to a future year of profit. Businesses carried out under sole proprietorships and general partnerships must be registered with the companies commission of malaysia. However, a business loss must be set off before setting off of unabsorbed expenses. Such loss can be carried forward for four years immediately succeeding the year in which the loss is incurred. Unabsorbed business losses may be carried forward indefinitely to offset against business income including companies with pioneer status, provided that the cessation of the period falls on or after 30 september 2005. Not a deemed business source), any unabsorbed capital allowance or adjusted losses can be carried forward. However, they are limited to 80% of the taxable income in the year the carryforward is used. 72) • loss can be set off only against business income. Unabsorbed losses and unabsorbed capital allowances can be carried forward to subsequent years until fully utilised. Losses which cannot be set off in the year of loss can be carried forward for set off in the subsequent years to some after any forward effects shall first be given for business losses and losses from speculation business before giving an effect of unabsorbed depreciation.

Related : Unabsorbed Business Loss Carried Forward Malaysia - Https Www Rsm Global Malaysia Insights Insights General Information Malaysian Taxation : In tabling the 2019 budget in parliament today, he announced that the review of tax treatment would be effective from year of assessment 2019..